Investments

Investments

What is the average investor returns?

What is the average investor returns?

I was in a conversation with a ex remisier..

He had been investing for the past 15yrs and has gotten no where when it comes to his investments.

He tried all kinds of investments, stocks, options funds and even forex.

His verdict:

I made lots of money. I also lost lots of money. After the very volatile 15yrs of his life, investing by himself gets him nowhere close to his goals.

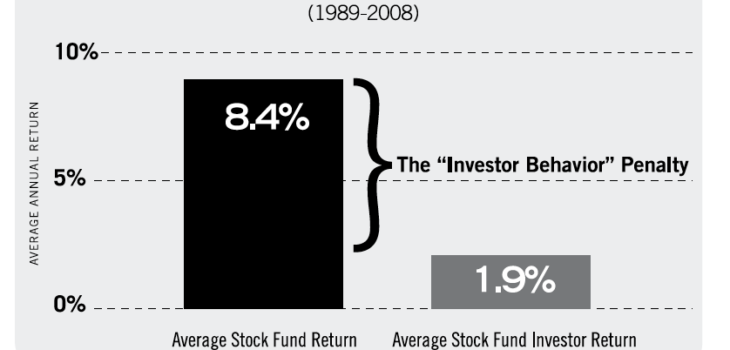

There is a study done that shows that average investors tend to underperform the market, largely due to one main reason – irrational human behaviour when it comes to investing which is multi faceted.

The human mind is designed not to make good decisions when it comes to investing. And that is the main reason for the huge gaps between the average investor and the actual market returns.

For those who have experienced it before and know about it, they will fall into various different traps from an emotional perspective.

There are 9 factors that cause an average investor to invest poorly.

If you would like to find out more, let me know and we can connect.

Speak with your experienced advisor so that you are confident of investing for the future.

Photo credits : Dalbar