Inspiration

Inspiration

Is there a reliable way to invest?

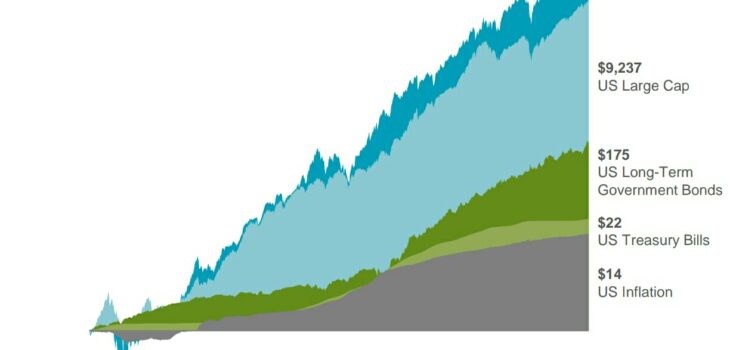

Investments and reliability hardly go hand in hand, I used to think. And investments are filled with ups and downs in the markets.

When I first started investing in 2005, I got excited. When I made that 10-20% return, I thought I should sell out before the markets go down. Sometimes I am right, sometimes I am not. And some of the time, that one wrong move will erase all gains made over the past few years.

Well, I had one objective – I needed to plan well for retirement for the long term which will be a few decades down the road. Is there a reliable way to get there especially since it is many years down the road?

My worries

What if I had invested and when I needed the money for retirement, the company I had invested into went out of business or is no longer a relevant business or unable to make the same profits? A few such companies may have been the recent SIA, Hyflux, Blackberry, Kodak etc.

Being able to predict accurately might have been due to skill or even luck at times. But to be able to do it right 100% of the time is almost impossible. Even Warren Buffet does not get it right all the time.

Investing on my own creates anxieties. Whenever I read the papers or look at my portfolio, I am tempted to make a trade. It is either to sell or buy and that creates additional stress for me that very day as I always hope to sell the highest or buy the lowest.

About 5 years ago, I have finally found a more reliable way to achieve my long goals with less emotions, less risk and yet higher expected returns, while building a large CORRETM portfolio. If you would like to find out more, you can send me a question.