Markets are at all time high

Now that markets are at all-time high, most speculators will probably feel very uncomfortable now. “What should the next step be? Should I sell, wait or top up?” How do I invest with a peace of mind?

For those who are invested into single stocks, seeing your stock go up sky high can be scary because you never know what might happen next. Some of these examples include Hyflux and Kodak or even SIA which could potentially have changed their future outlook.

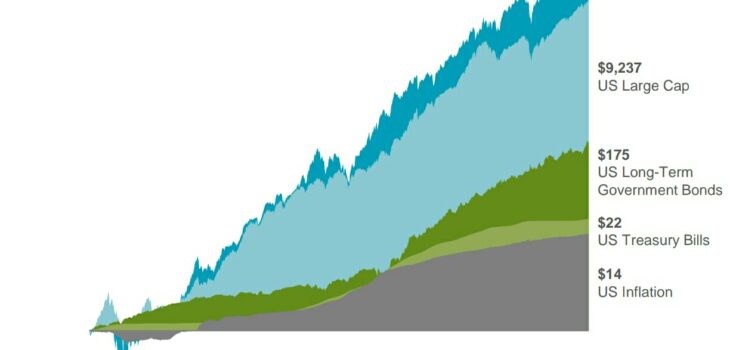

However, if you are a long term investor, looking back in history all the way back to evidence from year 1926, you would realize that the broad diversified markets always go up. And if an investor had just held a CORE asset allocated portfolio and rebalanced along the way, he would have been handsomely rewarded over the decades (as shown in the picture). Individual stocks would not have performed the same way. There are only a handful of stocks that might have been around for the same period of almost 100 years. Most of the individual stocks would either have been obsolete, closed down or disappeared over the years with the evolving markets and industries.

If we are building CORE portfolios that are broadly diversified across the world with proper rebalancing done over the years, it would be fair to say that the values in the future will be higher than it is today, whilst going through some crisis along the way (this is based on evidence investing).

If you would like to find out what CORE portfolios that can help you achieve your individual dreams and goals, whilst giving you peace of mind, you should always reach out to have a conversation.