Our brain is wired to lose money!

Do you know that our mind and brain is designed to lose money?

Imagine this with me. You are walking happily along the streets and suddenly, in front of you, there is a huge explosion! What is your first response? Is it to stand up and run towards the explosion? Or to duck down and run away from the explosion?

The amygdala or “the alarm” part of our brain reacts to fear, danger and real or perceived threats. It was designed to protect us from threats and regulates our emotional state.

Likewise, in a market crisis and stocks are falling, your brain’s initial response is to avoid the markets. This is called behavioural finance and our natural response to market crisis.

There was a survey done on participants with damaged amygdala who were invested during a market crisis. In fact, they were able to make better decisions when it came to investing before, during and after the crisis.

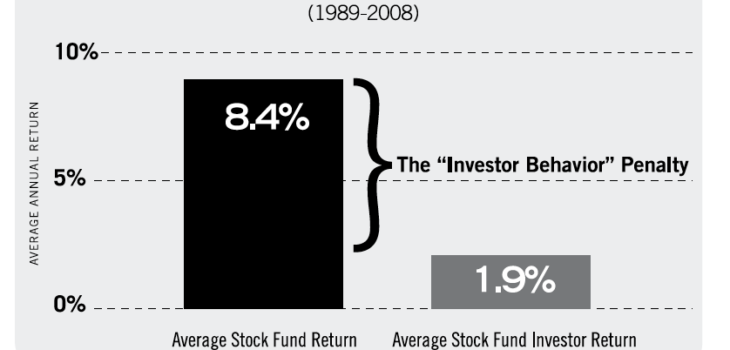

In short, our human brain is not designed to help us be successful in investing.

There are seasoned investors who have invested for many years and when the amount gets very large and the market falls are significant in the later years, wrong decisions are being made at the worst of times.

However, when you have a gatekeeper to keep your emotions in check, whilst trying to achieve your own long term personal goals, this helps to minimize the likelihood of emotional decision making. We are here as licensed financial advisors, who are gatekeepers for your wealth to ensure that you make sound decisions that do not detract you from your personal goals. On top of that, we help you make great decisions in times of crisis to build you further propel you towards your goals.